Please fill out the details below to receive information on Blue Wealth Events

"*" indicates required fields

Sydney property is internationally acclaimed as a blue-chip asset. Demand has buoyed the market to record highs, now reportedly being ‘the second least affordable market in the world’. Despite this, CoreLogic has shown that Sydney house prices dropped by -0.9% over the first quarter of 2018, and a -2.2% drop in the preceding one. This signalling the start of a Sydney market stagnation. However, many are still willing to invest substantial deposits to buy in Sydney, despite the market clearly passing its peak.

Let’s look at a case that will resonate with many – a mother living in Epping in Sydney’s North-West. Let’s call her Mary. Mary buys an investment property a couple of streets away from her house. She has the aim of holding onto the house so that her kids can more easily enter the local market in 20 years. After all, her property has done well, so why wouldn’t the next one.

This theory poses several questions, will Mary’s kids want to live in the same suburb when they grow up? Will they want to own a house in the future? Will they want to live closer to the city or the beach? Will they even live in Australia? It’s impossible to know, but it brings to light a trend that is commonly discussed here at Blue Wealth – people making investment decisions based on emotion alone.

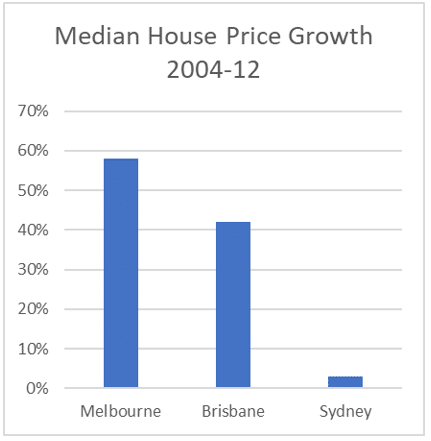

Sydney has performed strongly over the last six years, with most watching their family home grow in value faster than they could save their own money. However, people have forgotten about the period of stagnation that occurred from 2004-12 where the market remained at a virtual standstill.

Buyers would have been much better off investing in alternative markets over that period. Melbourne’s median house price grew by 58%, while Brisbane grew by 42%.

The hard truth is that in 2018, Mary from Epping could purchase outside of Sydney, with stronger opportunity for capital growth and help the kids get into the property market that way. That avoids the loaded risk (or hefty price tag) of buying after a market has peaked and at the beginning of a relatively long stagnation period.

Once Mary’s kids get older and need help getting into the market they’ve chosen to live in, she can sell the properties she bought and give them the money to help buy the property of their dreams.